|

|

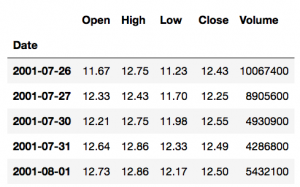

import numpy as np from pandas_datareader import data as wb import matplotlib.pyplot as plt AMZN = wb.DataReader('AMZN', data_source='google', start='2000-1-1') AMZN.head() |

|

|

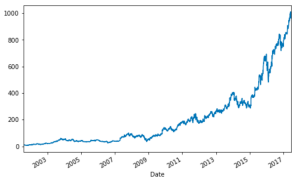

AMZN['Close'].plot(figsize=(8,5)) plt.show() |

Simple rate of return

rate of return = (ending price – beginning price) / beginning price

(P1 – P0) / P0 = P1 / P0 – 1

Use when dealing with multiple assets over the same timeframe.

|

|

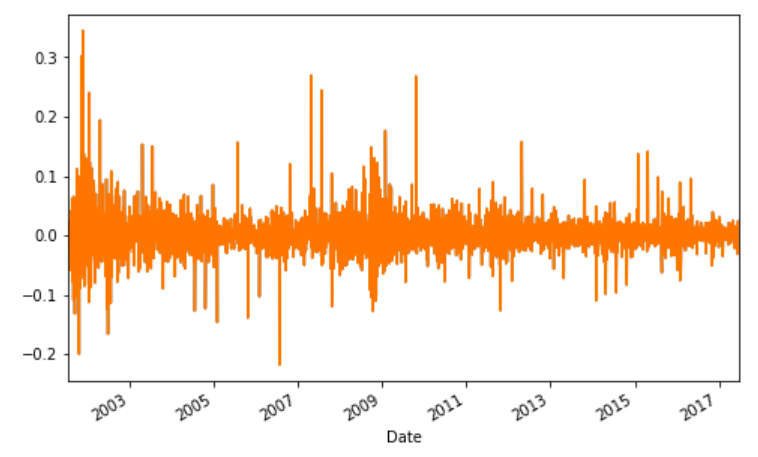

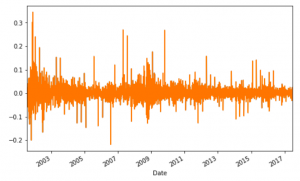

AMZN['simple_return'] = (AMZN['Close'] / AMZN['Close'].shift(1)) - 1 print (AMZN['simple_return']) |

Date

2001-07-26 NaN

2001-07-27 -0.014481

2001-07-30 0.024490

2001-07-31 -0.004781

2001-08-01 0.000801

2001-08-02 -0.024800

2001-08-03 -0.003281

2001-08-06 -0.020576

2001-08-07 -0.025210

2001-08-08 -0.042241

2001-08-09 -0.058506

2001-08-10 -0.048757

2001-08-13 0.017085

2001-08-14 0.040514

2001-08-15 -0.042735

2001-08-16 -0.026786

2001-08-17 0.018349

2001-08-20 0.041041

2001-08-21 -0.049038

2001-08-22 0.031345

2001-08-23 -0.055882

2001-08-24 0.062305

2001-08-27 -0.009775

2001-08-28 -0.015795

2001-08-29 -0.078235

2001-08-30 -0.054407

2001-08-31 0.028769

2001-09-04 -0.039150

2001-09-05 -0.109430

2001-09-06 0.065359

…

2017-05-10 -0.004062

2017-05-11 -0.001402

2017-05-12 0.014489

2017-05-15 -0.003516

2017-05-16 0.008455

2017-05-17 -0.022058

2017-05-18 0.014533

2017-05-19 0.001408

2017-05-22 0.011283

2017-05-23 0.000896

2017-05-24 0.009068

2017-05-25 0.013291

2017-05-26 0.002416

2017-05-30 0.000924

2017-05-31 -0.002087

2017-06-01 0.001337

2017-06-02 0.010824

2017-06-05 0.004579

2017-06-06 -0.008246

2017-06-07 0.007049

2017-06-08 0.000198

2017-06-09 -0.031635

2017-06-12 -0.013697

2017-06-13 0.016457

2017-06-14 -0.004405

2017-06-15 -0.012596

2017-06-16 0.024415

2017-06-19 0.007553

2017-06-20 -0.002593

2017-06-21 0.009712

Name: simple_return, Length: 4000, dtype: float64

|

|

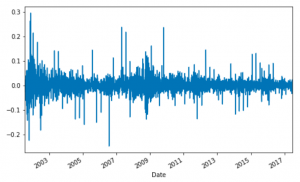

AMZN['simple_return'].plot(figsize=(8,5)) plt.show() |

|

|

avg_returns_d = AMZN['simple_return'].mean() avg_returns_d |

0.0015193424705951424

|

|

avg_returns_a = AMZN['simple_return'].mean() * 250 avg_returns_a |

0.3798356176487856

|

|

print (str(round(avg_returns_a, 5) * 100) + ' %') |

37.984 %

Logarithmic rate of return

ln(Pt / Pt-1)

10.0% = log $116 / $105 = log $116 – log $105

Use when you make calculations about a single asset over time.

|

|

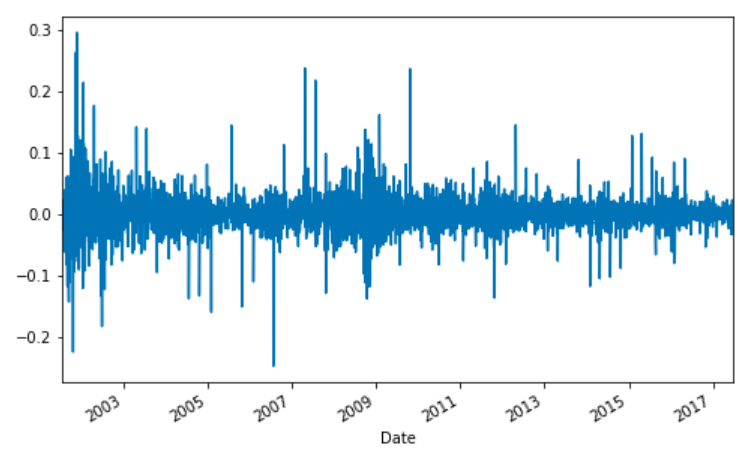

AMZN['log_return'] = np.log(AMZN['Close'] / AMZN['Close'].shift(1)) print (AMZN['log_return']) |

Date

2001-07-27 NaN

2001-07-30 0.024195

2001-07-31 -0.004792

2001-08-01 0.000800

2001-08-02 -0.025113

2001-08-03 -0.003287

2001-08-06 -0.020791

2001-08-07 -0.025533

2001-08-08 -0.043159

2001-08-09 -0.060287

2001-08-10 -0.049986

2001-08-13 0.016941

2001-08-14 0.039715

2001-08-15 -0.043675

2001-08-16 -0.027151

2001-08-17 0.018182

2001-08-20 0.040221

2001-08-21 -0.050282

2001-08-22 0.030864

2001-08-23 -0.057504

2001-08-24 0.060441

2001-08-27 -0.009823

2001-08-28 -0.015921

2001-08-29 -0.081465

2001-08-30 -0.055943

2001-08-31 0.028363

2001-09-04 -0.039937

2001-09-05 -0.115893

2001-09-06 0.063312

2001-09-07 0.043224

…

2017-05-11 -0.001403

2017-05-12 0.014385

2017-05-15 -0.003522

2017-05-16 0.008420

2017-05-17 -0.022305

2017-05-18 0.014428

2017-05-19 0.001407

2017-05-22 0.011220

2017-05-23 0.000896

2017-05-24 0.009027

2017-05-25 0.013204

2017-05-26 0.002413

2017-05-30 0.000923

2017-05-31 -0.002089

2017-06-01 0.001336

2017-06-02 0.010766

2017-06-05 0.004569

2017-06-06 -0.008281

2017-06-07 0.007024

2017-06-08 0.000198

2017-06-09 -0.032146

2017-06-12 -0.013792

2017-06-13 0.016324

2017-06-14 -0.004414

2017-06-15 -0.012676

2017-06-16 0.024122

2017-06-19 0.007524

2017-06-20 -0.002596

2017-06-21 0.009665

2017-06-22 -0.000928

Name: log_return, dtype: float64

|

|

AMZN['log_return'].plot(figsize=(8, 5)) plt.show() |

|

|

log_return_d = AMZN['log_return'].mean() log_return_d |

0.0010977419081520047

|

|

log_return_a = AMZN['log_return'].mean() * 250 log_return_a |

0.2744354770380012

|

|

print (str(round(log_return_a, 5) * 100) + ' %') |

27.444 %

Monte Carlo simulations

We are interested in observing the different possible realizations of a future event.

– Scenario 1

– Scenario 2

– Scenario 3

– Scenario 4

– Scenario 5

– Scenario 6

Historical data => A larger data set with “fictional” data

Current Revenues = Last Year Revenues * (1 + y-o-y growth rate)

– Revenue growth rate – Historical Data or User Intuition

– Revenue volatility – Historical Data or User Intuition

Cogs (Cost of Goods Sold): Modeled as a percentage of revenues

Opex: Modeled as a percentage of revenues

Revenues – Cogs = Gross Profit

Revenues – Opex = Operating Profit

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 |

import numpy as np import matplotlib.pyplot as plt rev_m = 170 rev_stdev = 20 iterations = 1000 rev = np.random.normal(rev_m, rev_stdev, iterations) rev plt.figure(figsize=(15,6)) plt.plot(rev) plt.show() COGS = - (rev * np.random.normal(0.6,0.1)) plt.figure(figsize=(15,6)) plt.plot(COGS) plt.show() COGS.mean() // -89.588838273282661 COGS.std() // 10.581370507673284 |

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 |

Gross_Profit = rev + COGS Gross_Profit plt.figure(figsize=(15,6)) plt.plot(Gross_Profit) plt.show() max(Gross_Profit) // 111.04813446627591 min(Gross_Profit) // 52.352121850588489 Gross_Profit.mean() // 80.688398780785718 Gross_Profit.std() // 9.5301363387028868 plt.figure(figsize=(10,6)) plt.hist(Gross_Profit, bins =[40,50,60,70,80,90,100,110,120]) plt.show() plt.figure(figsize=(10,6)) plt.hist(Gross_Profit, bins =20) plt.show() |

Asset pricing with Monte Carlo

Price Today = Price Yesterday * er

r: log return of share price between yesterday and today.

In(price today / price yesterday)

e.g. eIn(x) = x

Price Today = Price Yesterday * e

Logarithm Basics

log2(16) = x

2x = 16

x = 4

log100(1) = 0

1000 = 1

log2(2) = 1/3

81/3 = 2

log2(1/8) = -3

2-3 = 1/8

log8(1/2) = -1/3

8-1/3 = 1/81/3 = 1/2

Brownian motion

We can use Brownian motion in order to model r:

– Drift:

=> The direction rates of return have been headed in the past.

In(Current Price / Previous Price)

=> Calculate average, standard deviation and variance of daily returns in the historical period.

Drift = (μ – 1/2σ2)

Drift is the expected daily return of the stock.

– Volatility:

Random variable.

Random variable = σ * Z(Rand(0;1))

Price Today = Price Yesterday * eDrift + Random variable

Repeat the calculation 1,000 times.

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 |

import numpy as np import pandas as pd from pandas_datareader import data as wb import matplotlib.pyplot as plt from scipy.stats import norm %matplotlib inline ticker = 'AMZN' data = pd.DataFrame() data[ticker] = wb.DataReader(ticker, data_source = 'google', start='2007-1-1')['Close'] log_returns = np.log(1+data.pct_change()) log_returns.tail() data.plot(figsize=(10,6)) log_returns.plot(figsize=(10,6)) u=log_returns.mean() u // AMZN 0.001228 // dtype: float64 var = log_returns.var() var // AMZN 0.000635 // dtype: float64 drift = u - (0.5*var) drift // AMZN 0.00091 // dtype: float64 stdev = log_returns.std() stdev // AMZN 0.025207 // dtype: float64 |

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 |

type(drift) // pandas.core.series.Series type(stdev) // pandas.core.series.Series np.array(drift) // array([ 0.0009102]) // object.values: transfers the object into a numpy array drift.values // array([ 0.0009102]) stdev.values // array([ 0.02520659]) norm.ppf(0.95) // 1.6448536269514722 x = np.random.rand(10,2) x norm.ppf(x) z = norm.ppf(np.random.rand(10,2)) z t_intervals = 1000 iterations = 10 daily_returns = np.exp(drift.values + stdev.values * norm.ppf(np.random.rand(t_intervals, iterations))) daily_returns |

Euler’s Method

Differential equations introduction

yII + 2yI = 3y

fII(x) + 2fI(x) = 3f(x)

Leibniz’s notation

d2y / dx2 + 2 (dy / dx) = 3y

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 |

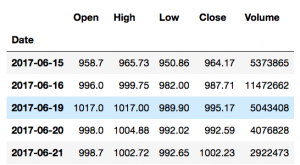

S0 = data.iloc[-1] S0 // AMZN 995.17 // Name: 2017-06-19 00:00:00, dtype: float64 price_list = np.zeros_like(daily_returns) price_list price_list[0] = 50 price_list for t in range(1, t_intervals): price_list[t] = price_list[t - 1]*daily_returns[t] price_list plt.figure(figsize=(10,6)) plt.plot(price_list) |

An Introduction to Derivative Contracts

A derivative is a financial instrument, whose price is derived based on the development of one or more underlying assets.

Originally, derivatives served as a hedging instrument.

– Hedging

– Speculating

– Aribtrageurs

Four Types of derivatives

– Forwards

Two parties agree that one party will sell to the other an underlying asset at a future point of time.

– Futures

Highly standardized forward contracts.

– Swaps

Two parties agree to exchange cash flows based on an underlying asset.

e.g. Interest rate, Stock Price, Bond Price, Commodity

– Options

An option contract enables its owner to buy or sell an underlying asset at a given price.

The Black Scholes formula

– A tool for derivatives pricing.

– calculates the value of an option.

– The holder of the option may decide he wants to buy the stock, but he may also decide he is better off without doing it. This freedom is valuable to every investor. Hence, it has a price.

A Call Option’s Payoff

– Strike Price vs. Share Price

– Share Price > Strike Price –> Exercise

– Strike Price > Share Price –> Don’t Exercise

The Black Scholes Formula

The Black Scholes formula calculates the value of a call by taking the difference between the amount you get if you exercise the option minus the amount you have to pay if you exercise the option.

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 |

import numpy as np import pandas as pd from pandas_datareader import data as wb from scipy.stats import norm def d1(S, K, r, stdev, T): return (np.log(S / K) + (r - stdev ** 2/2) * T) / (stdev * np.sqrt(T)) def d2(S, K, r, stdev, T): return (np.log(S / K) + (r - stdev ** 2/2) * T) / (stdev * np.sqrt(T)) norm.cdf(0) // 0.5 norm.cdf(0.25) // 0.5987063256829237 norm.cdf(0.75) // 0.77337264762313174 norm.cdf(9) // 1.0 def BSM(S, K, r, stdev, T): return (S*norm.cdf(d1(S, K, r, stdev, T))) - (K * np.exp(-r * T) * norm.cdf(d2(S, K, r, stdev, T))) ticker = 'AMZN' data = pd.DataFrame() data[ticker] = wb.DataReader(ticker, data_source='google', start='2007-1-1', end='2017-3-21')['Close'] S = data.iloc[-1] S // AMZN 843.2 // Name: 2017-03-21 00:00:00, dtype: float64 log_returns = np.log(1+data.pct_change()) stdev = log_returns.std()*250**0.5 stdev // AMZN 0.402353 // dtype: float64 r = 0.025 K = 110.0 T = 1 d1(S, K, r, stdev, T) // AMZN 4.922989 // dtype: float64 d2(S, K, r, stdev, T) // AMZN 4.922989 // dtype: float64 BSM(S, K, r, stdev, T) // AMZN 735.915596 // Name: 2017-03-21 00:00:00, dtype: float64 |

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 |

import numpy as np import pandas as pd from pandas_datareader import data as wb from scipy.stats import norm import matplotlib.pyplot as plt %matplotlib inline ticker = 'AMZN' data = pd.DataFrame() data[ticker] = wb.DataReader(ticker, data_source='google', start='2007-1-1', end='2007-3-21')['Close'] log_returns = np.log(1 + data.pct_change()) r = 0.025 stdev = log_returns.std() * 250 ** 0.5 stdev // AMZN 0.28593 // dtype: float64 type(stdev) // pandas.core.series.Series stdev = stdev.values stdev // array([ 0.28592956]) T=1.0 t_intervals = 250 delta_t = T / t_intervals iterations = 10000 Z = np.random.standard_normal((t_intervals + 1, iterations)) S = np.zeros_like(Z) S0 = data.iloc[-1] S[0] = S0 for t in range(1, t_intervals + 1): S[t]=S[t-1] * np.exp((r - 0.5 * stdev ** 2) * delta_t + stdev * delta_t ** 0.5 * Z[t]) S S.shape // (251, 10000) plt.figure(figsize=(10,6)) plt.plot(S[:,:10]) |

|

|

p = np.maximum(S[-1] - 110, 0) p // array([ 0., 0., 0., ..., 0., 0., 0.]) p.shape // (10000,) C = np.exp(-r * T) * np.sum(p) / iterations C // 0.0 |

Multivariate Regressions

Yi = β0 + β1X1 + β2X2 + βiXi + εi

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 |

import numpy as np import pandas as pd from scipy import stats import statsmodels.api as sm import matplotlib.pyplot as plt data = pd.read_excel('[PATH]/Housing.xlsx') data // Multivariate Regression: // Independent Variables: "House Size (sq.ft.)", "Number of Rooms", "Year of Construction" X = data[['House Size (sq.ft.)', 'Number of Rooms', 'Year of Construction']] Y = data['House Price'] X1 = sm.add_constant(X) reg = sm.OLS(Y,X1).fit() reg.summary() // Independent Variables: 'House Size (sq.ft.)', 'Number of Rooms' X = data[['House Size (sq.ft.)', 'Number of Rooms']] Y = data['House Price'] X1 = sm.add_constant(X) reg = sm.OLS(Y, X1).fit() reg.summary() |

The Capital Asset Pricing Model (CAPM)

According to Markowitz, in the CAPM investors are:

– risk-averse

– prefer higher returns

– willing to buy the optimal portfolio

The market portfolio:

– a combination of all the possible investments in the world.

The risk-free asset:

– the CAPM assumes the existence of a risk-free asset.

– an investment with zero risk.

– Why should we assume the risk-free rate has a lower expected rate of return?

=> In efficient markets, investors are only compensated for the added risk they are willing to bear.

The Capital Market Line

– investors will allocate their money between the risk-free and the market portfolio

In the CAPM, investors will invest in:

– depending on their risk preferences, they will choose to buy more of the risk-free asset or more of the market portfolio.

Beta

β = Cov(rx, rm) / σm2

– measures the market risk that cannot be avoided through diversification.

β = 0: No relationship

β < 1: Defensive (Walmart)

β > 1: Aggressive (Ford)

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 |

import numpy as np import pandas as pd from pandas_datareader import data as wb tickers = ['AMZN','S&P 500'] data = pd.DataFrame() for t in tickers: data[t] = wb.DataReader(t, data_source='google', start='2012-1-1',end='2016-12-31')['Close'] sec_returns = np.log(data/data.shift(1)) cov = sec_returns.cov() * 250 cov cov_with_market = cov.iloc[0,1] cov_with_market // 0.0039599527224196103 market_var = sec_returns['S&P 500'].var() * 250 market_var // 0.02393760982543131 // Beta: AMZN_beta = cov_with_market / market_var AMZN_beta // 0.16542807537169221 |

The Capital Asset Pricing Model

ri = rf + βim(rm – rf)

rf: risk-free

βim: beta between the stock and the market

rm: market return

Risk-free: Approximate with 10-year US government bond yield: 2.5%

Beta: Approximate the market portfolio with the S&P500: 0.62

Equity Risk Premium: Historically, it has been between 4.5% and 5.5%

r(i) = 2.5% + 0.62 * 5% = 5.6%

|

|

// Calculate the expected return of AMZN(CAPM): AMZN_er = 0.025 + AMZN_beta * 0.05 AMZN_er // 0.033271403768584611 |

Sharpe Ratio

William Sharpe

Sharpe Ratio = (ri – rf) / σi

rf: risk-free rate

ri: rate of return of the stock “i”

σi: standard deviation of the stock “i”

|

|

// Sharpe ratio: Sharpe = (AMZN_er - 0.025) / (sec_returns['AMZN'].std() * 250 ** 0.5) Sharpe // 0.02701837714000498 |

Alpha

The Capital Asset Pricing Model:

ri = α + rf + βim(rm – rf)

– The standard CAPM setting assumes an alpha equal to 0.

– We can only compare the alpha of investments with a similar risk profile.

Portfolio Theory

1952, Harry Markowitz published a paper.

– investors should understand the relationship between securities in their portfolio.

Implementation

|

|

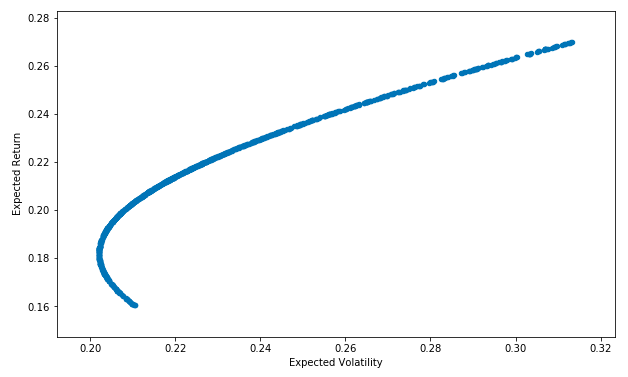

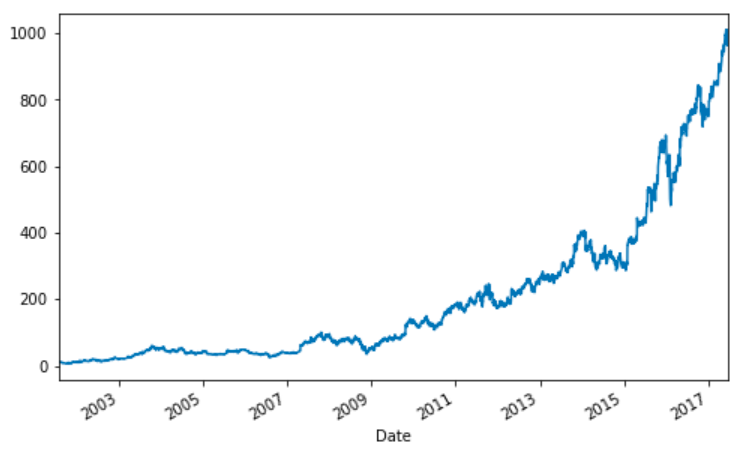

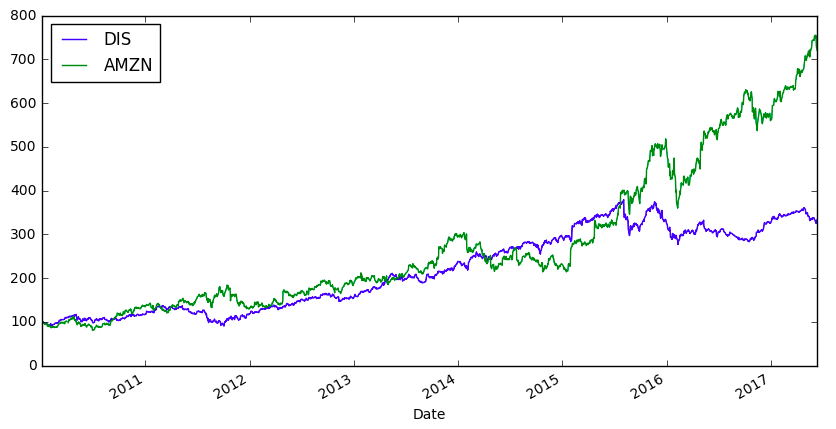

import numpy as np import pandas as pd from pandas_datareader import data as wb import matplotlib.pyplot as plt %matplotlib inline assets = ['DIS', 'AMZN'] pf_data = pd.DataFrame() for a in assets: pf_data[a] = wb.DataReader(a, data_source = 'google', start = '2010-1-1')['Close'] pf_data.tail() (pf_data / pf_data.iloc[0] * 100).plot(figsize=(10,5)) |

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 |

log_returns = np.log(pf_data / pf_data.shift(1)) log_returns.mean() * 250 // DIS 0.160962 // AMZN 0.268312 // dtype: float64 log_returns.cov() * 250 log_returns.corr() num_assets = len(assets) num_assets // 2 arr = np.random.random(2) arr // array([ 0.52831474, 0.47945205]) arr[0] + arr[1] // 1.0077667888401995 weights = np.random.random(num_assets) weights /= np.sum(weights) weights // array([ 0.47348175, 0.52651825]) weights[0] + weights[1] // 1.0 |

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 |

// Expected Portfolio Return: np.sum(weights * log_returns.mean()) * 250 // 0.2496822910761077 // Expected Portfolio Variance: np.dot(weights.T, np.dot(log_returns.cov() * 250, weights)) // 0.074759086518318432 // Expected Portfolio Volatility: np.sqrt(np.dot(weights.T,np.dot(log_returns.cov() * 250, weights))) // 0.27342107914043212 pfolio_returns = [] pfolio_volatilities = [] for x in range (1000): weights = np.random.random(num_assets) weights /= np.sum(weights) pfolio_returns.append(np.sum(weights * log_returns.mean()) * 250) pfolio_volatilities.append(np.sqrt(np.dot(weights.T,np.dot(log_returns.cov() * 250, weights)))) pfolio_returns, pfolio_volatilities pfolio_returns = [] pfolio_volatilities = [] for x in range (1000): weights = np.random.random(num_assets) weights /= np.sum(weights) pfolio_returns.append(np.sum(weights * log_returns.mean()) * 250) pfolio_volatilities.append(np.sqrt(np.dot(weights.T,np.dot(log_returns.cov() * 250, weights)))) pfolio_returns = np.array(pfolio_returns) pfolio_volatilities = np.array(pfolio_volatilities) pfolio_returns, pfolio_volatilities portfolios = pd.DataFrame({'Return': pfolio_returns, 'Volatility': pfolio_volatilities}) portfolios.head() portfolios.tail() portfolios.plot(x='Volatility', y='Return', kind='scatter', figsize=(10,6)); plt.xlabel('Expected Volatility') plt.ylabel('Expected Return') |