Python Tools

Adjusted Closing Price

Adjusted Closing Price

http://www.investopedia.com/terms/a/adjusted_closing_price.asp

How do I calculate the adjusted closing price for a stock?

http://www.investopedia.com/ask/answers/06/adjustedclosingprice.asp

Data Analysis and Visualization: Stock Market Analysis

Reference

Moving Average – MA

http://www.investopedia.com/terms/m/movingaverage.asp

How To Use A Moving Average To Buy Stocks

http://www.investopedia.com/articles/active-trading/052014/how-use-moving-average-buy-stocks.asp

Pearson correlation coefficient

http://en.wikipedia.org/wiki/Pearson_product-moment_correlation_coefficient

Annotating Axes: matplotlib

http://matplotlib.org/users/annotations_guide.html

Quantile

https://en.wikipedia.org/wiki/Quantile

Monte Carlo Simulation With GBM

http://www.investopedia.com/articles/07/montecarlo.asp

The Rate of Return of Amazon’s Stock Price

|

1 2 3 4 5 6 7 |

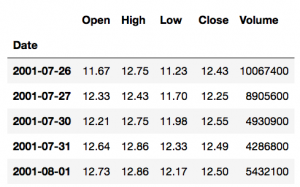

import numpy as np from pandas_datareader import data as wb import matplotlib.pyplot as plt AMZN = wb.DataReader('AMZN', data_source='google', start='2000-1-1') AMZN.head() |

|

1 |

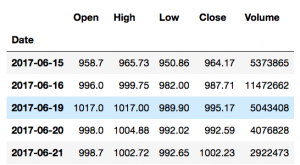

AMZN.tail() |

|

1 2 |

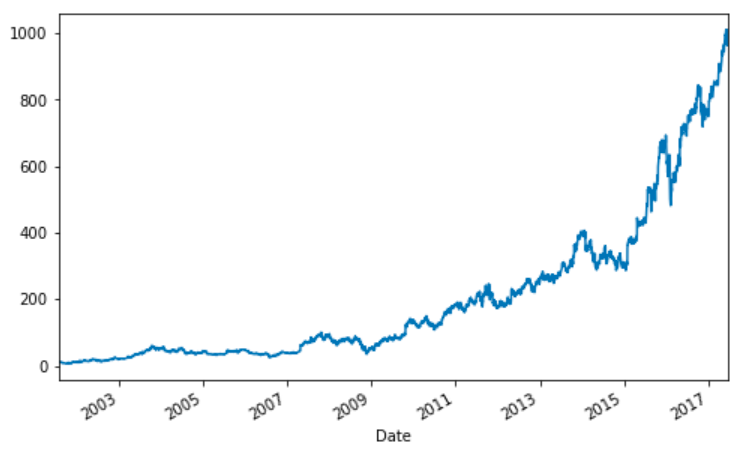

AMZN['Close'].plot(figsize=(8,5)) plt.show() |

Simple rate of return

rate of return = (ending price – beginning price) / beginning price

(P1 – P0) / P0 = P1 / P0 – 1

Use when dealing with multiple assets over the same timeframe.

|

1 2 |

AMZN['simple_return'] = (AMZN['Close'] / AMZN['Close'].shift(1)) - 1 print (AMZN['simple_return']) |

Date

2001-07-26 NaN

2001-07-27 -0.014481

2001-07-30 0.024490

2001-07-31 -0.004781

2001-08-01 0.000801

2001-08-02 -0.024800

2001-08-03 -0.003281

2001-08-06 -0.020576

2001-08-07 -0.025210

2001-08-08 -0.042241

2001-08-09 -0.058506

2001-08-10 -0.048757

2001-08-13 0.017085

2001-08-14 0.040514

2001-08-15 -0.042735

2001-08-16 -0.026786

2001-08-17 0.018349

2001-08-20 0.041041

2001-08-21 -0.049038

2001-08-22 0.031345

2001-08-23 -0.055882

2001-08-24 0.062305

2001-08-27 -0.009775

2001-08-28 -0.015795

2001-08-29 -0.078235

2001-08-30 -0.054407

2001-08-31 0.028769

2001-09-04 -0.039150

2001-09-05 -0.109430

2001-09-06 0.065359

…

2017-05-10 -0.004062

2017-05-11 -0.001402

2017-05-12 0.014489

2017-05-15 -0.003516

2017-05-16 0.008455

2017-05-17 -0.022058

2017-05-18 0.014533

2017-05-19 0.001408

2017-05-22 0.011283

2017-05-23 0.000896

2017-05-24 0.009068

2017-05-25 0.013291

2017-05-26 0.002416

2017-05-30 0.000924

2017-05-31 -0.002087

2017-06-01 0.001337

2017-06-02 0.010824

2017-06-05 0.004579

2017-06-06 -0.008246

2017-06-07 0.007049

2017-06-08 0.000198

2017-06-09 -0.031635

2017-06-12 -0.013697

2017-06-13 0.016457

2017-06-14 -0.004405

2017-06-15 -0.012596

2017-06-16 0.024415

2017-06-19 0.007553

2017-06-20 -0.002593

2017-06-21 0.009712

Name: simple_return, Length: 4000, dtype: float64

|

1 2 |

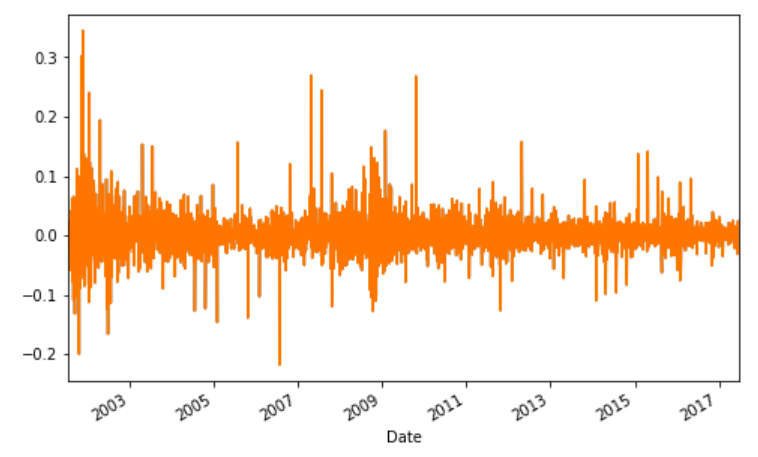

AMZN['simple_return'].plot(figsize=(8,5)) plt.show() |

|

1 2 |

avg_returns_d = AMZN['simple_return'].mean() avg_returns_d |

0.0015193424705951424

|

1 2 |

avg_returns_a = AMZN['simple_return'].mean() * 250 avg_returns_a |

0.3798356176487856

|

1 |

print (str(round(avg_returns_a, 5) * 100) + ' %') |

37.984 %

Logarithmic rate of return

ln(Pt / Pt-1)

10.0% = log $116 / $105 = log $116 – log $105

Use when you make calculations about a single asset over time.

|

1 2 |

AMZN['log_return'] = np.log(AMZN['Close'] / AMZN['Close'].shift(1)) print (AMZN['log_return']) |

Date

2001-07-27 NaN

2001-07-30 0.024195

2001-07-31 -0.004792

2001-08-01 0.000800

2001-08-02 -0.025113

2001-08-03 -0.003287

2001-08-06 -0.020791

2001-08-07 -0.025533

2001-08-08 -0.043159

2001-08-09 -0.060287

2001-08-10 -0.049986

2001-08-13 0.016941

2001-08-14 0.039715

2001-08-15 -0.043675

2001-08-16 -0.027151

2001-08-17 0.018182

2001-08-20 0.040221

2001-08-21 -0.050282

2001-08-22 0.030864

2001-08-23 -0.057504

2001-08-24 0.060441

2001-08-27 -0.009823

2001-08-28 -0.015921

2001-08-29 -0.081465

2001-08-30 -0.055943

2001-08-31 0.028363

2001-09-04 -0.039937

2001-09-05 -0.115893

2001-09-06 0.063312

2001-09-07 0.043224

…

2017-05-11 -0.001403

2017-05-12 0.014385

2017-05-15 -0.003522

2017-05-16 0.008420

2017-05-17 -0.022305

2017-05-18 0.014428

2017-05-19 0.001407

2017-05-22 0.011220

2017-05-23 0.000896

2017-05-24 0.009027

2017-05-25 0.013204

2017-05-26 0.002413

2017-05-30 0.000923

2017-05-31 -0.002089

2017-06-01 0.001336

2017-06-02 0.010766

2017-06-05 0.004569

2017-06-06 -0.008281

2017-06-07 0.007024

2017-06-08 0.000198

2017-06-09 -0.032146

2017-06-12 -0.013792

2017-06-13 0.016324

2017-06-14 -0.004414

2017-06-15 -0.012676

2017-06-16 0.024122

2017-06-19 0.007524

2017-06-20 -0.002596

2017-06-21 0.009665

2017-06-22 -0.000928

Name: log_return, dtype: float64

|

1 2 |

AMZN['log_return'].plot(figsize=(8, 5)) plt.show() |

|

1 2 |

log_return_d = AMZN['log_return'].mean() log_return_d |

0.0010977419081520047

|

1 2 |

log_return_a = AMZN['log_return'].mean() * 250 log_return_a |

0.2744354770380012

|

1 |

print (str(round(log_return_a, 5) * 100) + ' %') |

27.444 %